In today’s hypercompetitive investment landscape, active investment managers must earn their fees by targeting genuine opportunities to outperform. To do this, managers need to use strategies that are different from those of other investors. If an active manager is doing something different, it should be evident in the results. Genuine active managers will tend to have high active share, meaning they stand apart from the broad market “herd.”

Beyond a genuine shot at outperformance, a truly active strategy also displays a low correlation with passive strategies. Strategies with positive expected returns and low correlations to other opportunities help make portfolios more resilient in a variety of environments.

Counterpoint’s alternative equity strategies aim to target genuine alpha compared with a simple market model. The active share in our market-neutral strategies is 100%, and our risk management approach seeks to neutralize most broad macro risks, reducing correlations with many other investment strategies.

Of course, no strategy outperforms in all environments, and systematic factor-based strategies have faced real challenges in the recent year. Despite this, we believe that endurance of short-term pain is rewarded with excess returns in the long run. If it were easy all the time, everyone would be doing it, and factor-based strategies’ rewards would likely diminish. We believe there are two keys to successful implementation of factor-based strategies: 1) include a factor-based strategy as one component of a total diversified portfolio; and 2) focus on longer-term results while making sure the strategy is performing according to its design.

Our Core Strategy

Counterpoint’s equity investment philosophy is driven by two core beliefs:

- Persistent human psychological biases cause some stocks to become overvalued and others to become undervalued. (Mispricings driven by psychological biases are known as “factors” or “anomalies.”)

- A systematic strategy that finds mispriced stocks is the most efficient way to profit from the human error that causes mispricings.

These beliefs aren’t controversial. Almost any strategy that does not invest passively in an index like the S&P 500 is driven by a belief in mispricings driven by human investor error. The rise of “smart beta” strategies in recent years is driven by a belief in a systematic approach to profiting from those errors.

Although our core beliefs are reasonably widely held, the way we act on our beliefs is less common.

The Benefits of Short-Selling

The past decade has shown that it’s not enough to find underpriced stocks and buy them in a long-only portfolio. Long-only “smart beta” funds have helped crowd out factor-based opportunities for buyers of stocks. (For more on this subject, please see “Where Did All the Alpha Go?“)

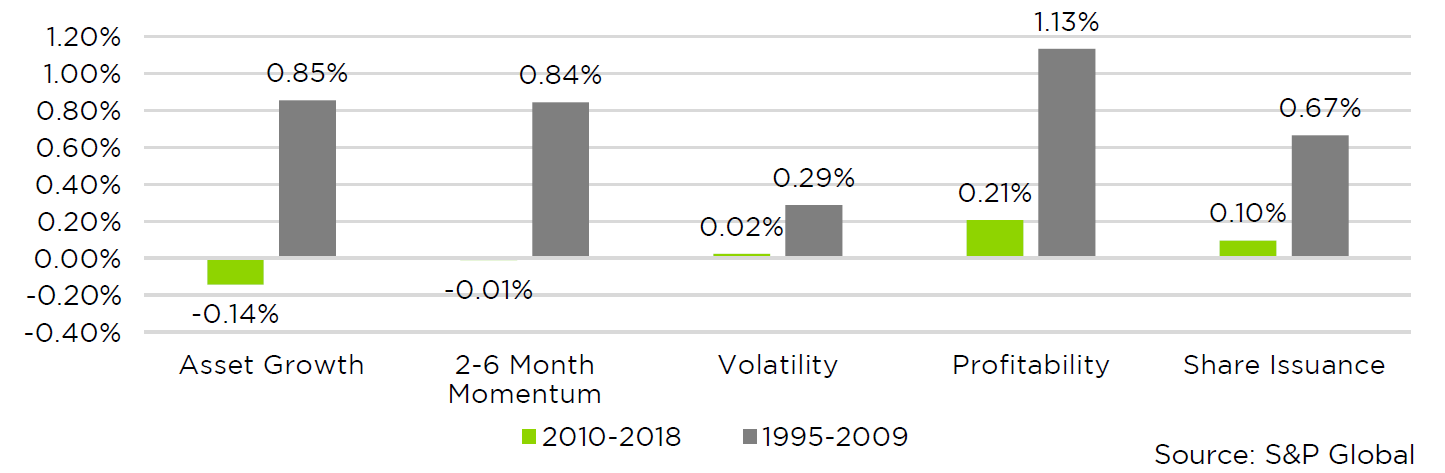

Long-Only Top Decile Factor Exposure Monthly Performance Relative to the S&P 500

Simply buying underpriced stocks based on factors hasn’t been very rewarding in recent years. Stocks with the greatest positive factor exposure to some common anomalies have shown limited outperformance relative to the S&P 500 index during the recent market cycle.

While factor based investing has become crowded on the long side, far fewer strategies are able or willing to sell stocks short. (A short sale enables an investor to benefit when a stock goes down.) There are still many opportunities for investors who sell short overpriced stocks. In fact, that’s where most of the opportunities remain for factor-based strategies.

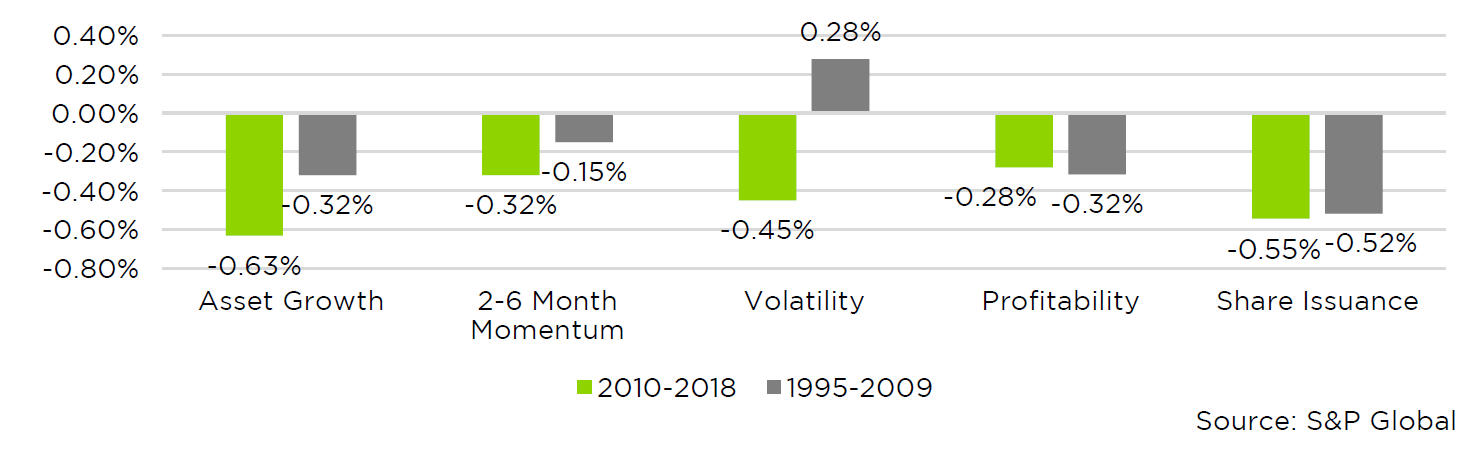

Short-Only Bottom Decile Factor Exposure Monthly Performance Relative to the S&P 500

Stocks with the greatest inverse exposure to some common anomalies have underperformed in the most recent cycle, suggesting that there is still a benefit to shorting stocks with poor anomaly exposure.

Counterpoint’s equity strategies sell stocks short to capture the persistent overpricing of some stocks. Many other systematic strategies lack this key tool.

More Opportunities in Small Companies

Competition among investors is fiercest among larger companies, which tend to be represented in more portfolios and which receive more media and Wall Street analyst coverage. The additional effort investors put into researching large companies makes it more difficult to find mispricings. This creates another hurdle for many systematic anomaly-driven strategies.

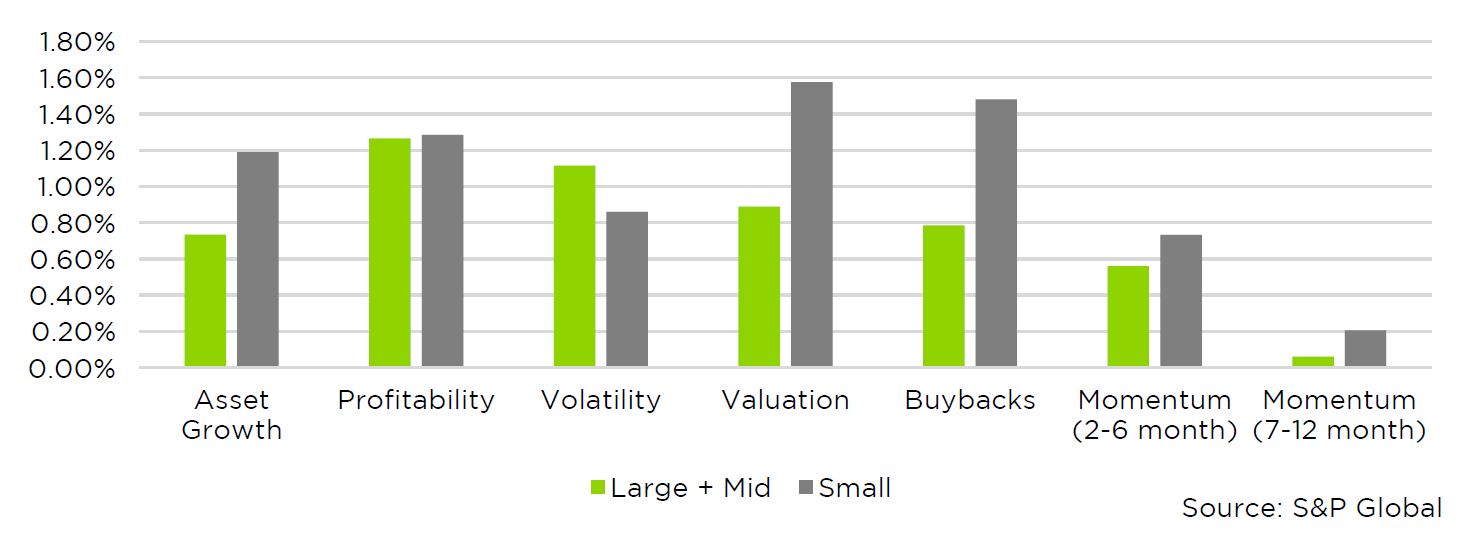

Anomaly Factor Returns to Global Small – and Large-Cap Stocks, 2000-2018

Monthly arithmetic mean returns to long-short portfolios of global stocks are pictured above. Each factor portfolio is long (short) the top (bottom) decile of stocks as ranked by factor exposure.

Counterpoint’s equity strategies have meaningful exposure to smaller companies – generally more than 50% of its portfolios are invested in small-caps. This creates greater opportunity to capitalize on mispricings in this less-examined area of the stock market. (We discuss this in more depth in “Bigger Isn’t Always Better.”)

International Investing

Although factor-based strategies work globally, some have lately done better when applied outside the U.S. than they have at home.

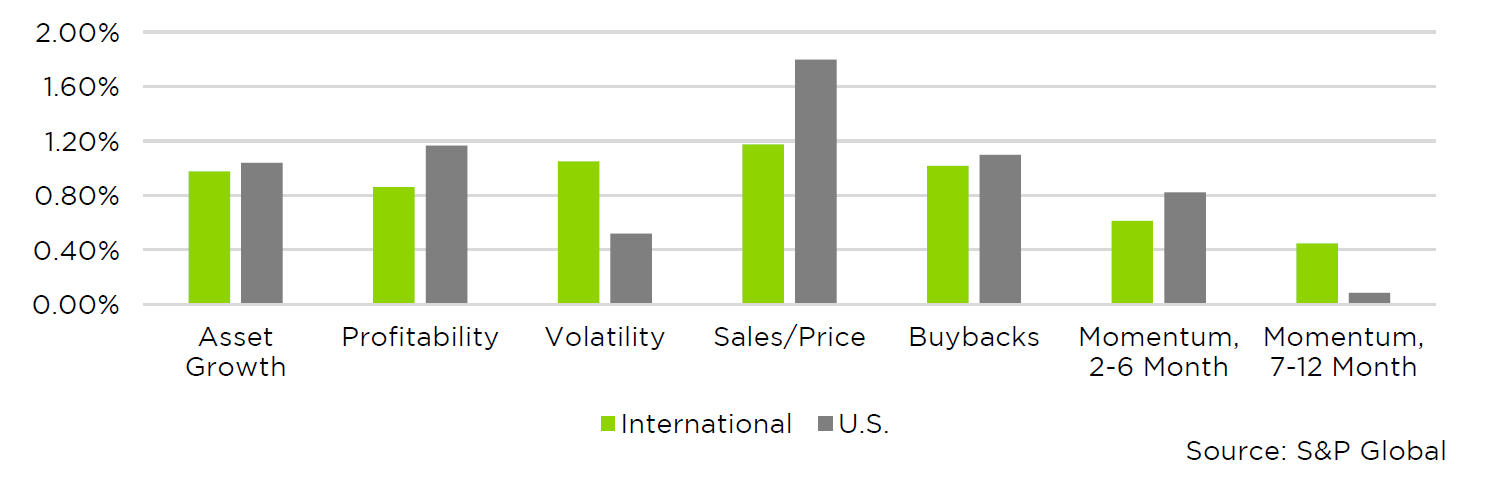

Investment Anomaly Returns, 2000-2018

The likely explanation is similar to the one for greater price efficiency in larger companies: A large portion of the world’s investment capital is in the U.S., and investors are more likely to look to their home countries for opportunities. This home-country bias creates an opportunity for investors who are willing to look abroad, particularly those willing to pursue market-neutral approaches like Counterpoint’s. Additionally, the robust media and financial analysis infrastructure in the U.S. helps price domestic companies more efficiently. (There’s more on this subject in “Where Factor Investing Has Worked.”)

Managing Risk

Counterpoint applies two key risk-management techniques that distinguish our approach.

First, while we believe that most of the factor-based opportunities are only available to strategies that include short selling, we maintain a portfolio that includes both longs and shorts. Exposure to both the long and short side of the market also makes it possible to better manage market risk.

Second, we aim to neutralize sector, country, and market risk exposure in our stock selection model. For example, when we find opportunities in specific oil companies, we manage the portfolio to avoid exposure to risks that face the oil industry as a whole. The same applies to the technology sector, consumer goods, other industries, and other countries. By managing these risks, we aim to derive returns primarily from the human psychological errors that drive our investment philosophy.

Conclusion

Counterpoint’s equity strategies seek to provide a distinct approach to the financial markets. We measure and aim for a highly active strategy with low correlation to the broad market “herd.” We also deploy the necessary tactics to succeed with a factor-based strategy: We sell short; we target smaller companies; and we invest internationally.

We believe this philosophy can lead to reduced portfolio volatility while seeking competitive investment returns, resulting in a strong long-term risk-reward profile. We take seriously our responsibility to find genuine mispricing in equity markets; we measure and manage the types of risks we take; and we aim to add genuine value to investor portfolios over time.