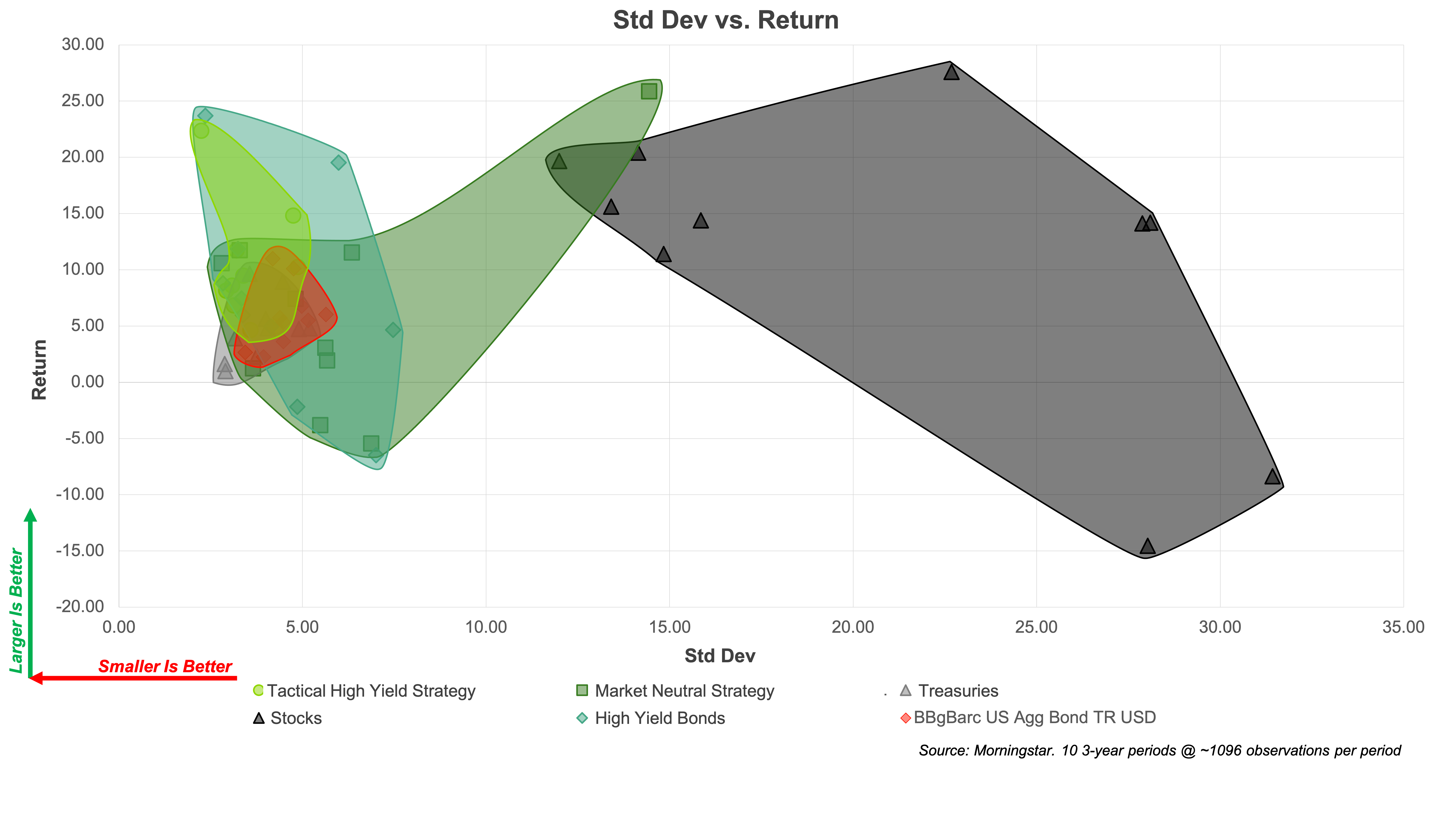

Std Dev vs. Return

Source: Morningstar. Displayed above are the standard deviation and return of different asset classes using the S&P 500 Total Return Index to represent “Stocks”, Morningstar US Fund High Yield Bond Category to represent “High Yield Bonds”, Morningstar US Fund Intermediate Government to represent “Treasuries,” and the Bloomberg Barclays US Aggregate Bond Index. Source: Kenneth French Data Library. The 3 Factor Market Neutral Strategy delivers the risk-free rate plus the simple average of returns to value, profitability, and momentum portfolios. Each factor portfolio is long the ⅓ of all stocks with the greatest factor exposure and short the ⅓ of stocks with the lowest factor exposure. The model multifactor portfolio is neither optimized for risk-adjusted returns nor does it improve stock selection with an aggregate model. Multifactor portfolio returns include the long-run risk free rate and do not factor in transaction costs, variables that would drag on returns. The High Yield Strategy is defined by buying the Morningstar High Yield Category when it closes above its 200-day moving average the prior day. The strategy entirely switches to exposure of the Bloomberg U.S. Treasury 3-5 Year Total Return Index when the Morningstar High Yield Category closes below its 200-day moving average.

Source: Morningstar. Displayed above are the standard deviation and return of different asset classes using the S&P 500 Total Return Index to represent “Stocks”, Morningstar US Fund High Yield Bond Category to represent “High Yield Bonds”, Morningstar US Fund Intermediate Government to represent “Treasuries,” and the Bloomberg Barclays US Aggregate Bond Index. Source: Kenneth French Data Library. The 3 Factor Market Neutral Strategy delivers the risk-free rate plus the simple average of returns to value, profitability, and momentum portfolios. Each factor portfolio is long the ⅓ of all stocks with the greatest factor exposure and short the ⅓ of stocks with the lowest factor exposure. The model multifactor portfolio is neither optimized for risk-adjusted returns nor does it improve stock selection with an aggregate model. Multifactor portfolio returns include the long-run risk free rate and do not factor in transaction costs, variables that would drag on returns. The High Yield Strategy is defined by buying the Morningstar High Yield Category when it closes above its 200-day moving average the prior day. The strategy entirely switches to exposure of the Bloomberg U.S. Treasury 3-5 Year Total Return Index when the Morningstar High Yield Category closes below its 200-day moving average.

There is no guarantee that any investment strategy will achieve its objectives, generate profits or avoid losses. The indices shown are for informational purposes only and are not reflective of any investment. As it is not possible to invest in the indices, the data shown does not reflect or compare features of an actual investment, such as its objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features. Past performance is no guarantee of future results.

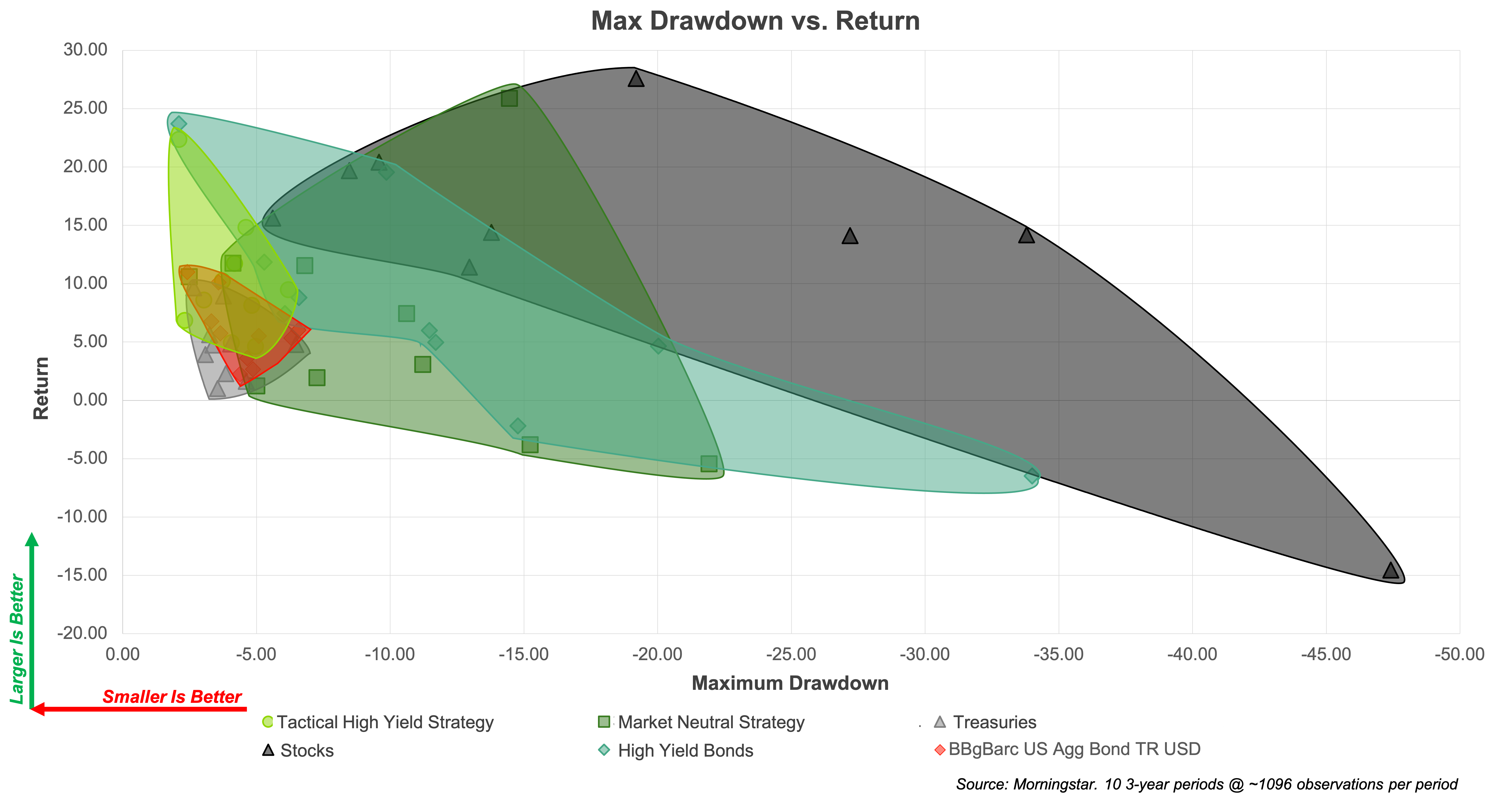

Max Drawdown vs. Return

Source: Morningstar. Displayed above are the max drawdown and return of different asset classes using the S&P 500 Total Return Index to represent “Stocks”, Morningstar US Fund High Yield Bond Category to represent “High Yield Bonds”, Morningstar US Fund Intermediate Government to represent “Treasuries,” and the Bloomberg Barclays US Aggregate Bond Index. Source: Kenneth French Data Library. The 3 Factor Market Neutral Strategy delivers the risk-free rate plus the simple average of returns to value, profitability, and momentum portfolios. Each factor portfolio is long the ⅓ of all stocks with the greatest factor exposure and short the ⅓ of stocks with the lowest factor exposure. The model multifactor portfolio is neither optimized for risk-adjusted returns nor does it improve stock selection with an aggregate model. Multifactor portfolio returns include the long-run risk free rate and do not factor in transaction costs, variables that would drag on returns. The High Yield Strategy is defined by buying the Morningstar High Yield Category when it closes above its 200-day moving average the prior day. The strategy entirely switches to exposure of the Bloomberg U.S. Treasury 3-5 Year Total Return Index when the Morningstar High Yield Category closes below its 200-day moving average.

There is no guarantee that any investment strategy will achieve its objectives, generate profits or avoid losses. The indices shown are for informational purposes only and are not reflective of any investment. As it is not possible to invest in the indices, the data shown does not reflect or compare features of an actual investment, such as its objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features. Past performance is no guarantee of future results.