As of March 11, 2026, year-to-date factor performance has been characterized by strong momentum leadership, improving quality exposure in developed markets, and persistent underperformance of defensive and valuation factors, with regional dispersion particularly evident in Asia. The Counterpoint Factor Scoreboard1 factor spread charts (Q5 minus Q1 quintile returns) highlight a market regime where trend persistence and earnings revisions dominate, while low-risk and valuation signals have lagged significantly.

These dynamics suggest the market environment in early 2026 has favored trend-following and sentiment driven strategies, while stability and valuation-driven allocations have struggled in the current risk-seeking market regime.

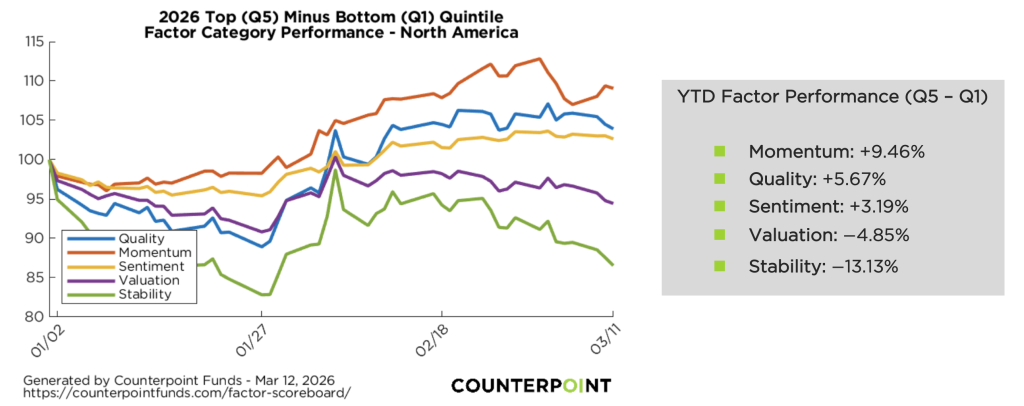

North America

North American markets show clear momentum leadership, with the momentum factor producing a ~9.5% spread between the top and bottom quintiles, the strongest factor signal across all regions. This result suggests that recent winners have continued to outperform laggards, consistent with a market environment driven by earnings revisions, AI-related technology leadership, and persistent sector trends.

Quality also delivered strong performance, generating a 5.7% spread, indicating investor preference for companies with stronger profitability and balance sheet characteristics. The quality factor typically emphasizes firms with high return on equity, stable earnings growth, and lower leverage, attributes that tend to outperform during periods of macro uncertainty.

In contrast, valuation and stability factors lagged, with North American low-risk stability factor posting the worst performance of any factor globally at −13.13%. This reflects a continued shift toward higher beta and cyclical exposures, where investors favor growth-oriented equities rather than defensive, low-volatility stocks.

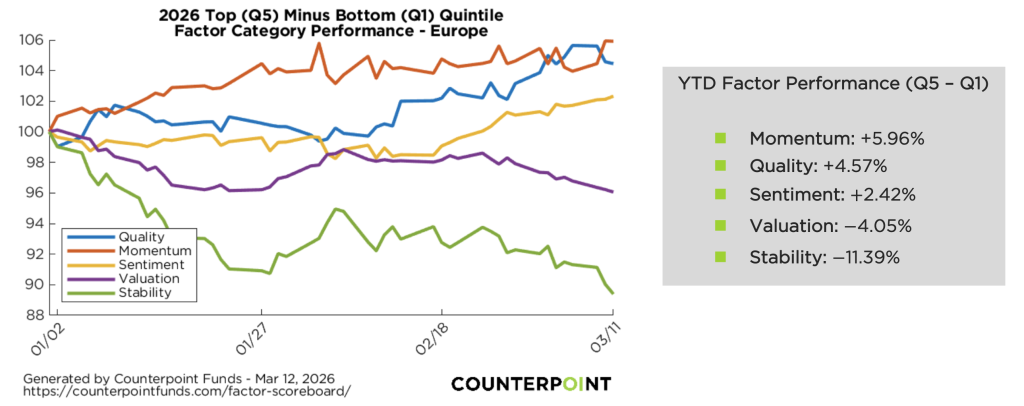

Europe

European factor performance broadly mirrors North America but with slightly more moderate dispersion among the factors. Momentum again leads, generating a nearly 6% return, as recent winner stocks have continued to win and recent loser stocks have continued to lose, confirming the persistence of cross-sectional price trends among European equities. Quality also delivered positive results, indicating that firms with stronger financial fundamentals and profitability characteristics have outperformed weaker peers.

As in North America, valuation factors struggled in Europe, with cheaper stocks underperforming higher-multiple peers. This dynamic reflects a continuation of the global pattern in which growth and earnings momentum remain dominant market drivers. The stability factor again underperformed significantly, highlighting the ongoing rotation away from low-volatility defensive equities.

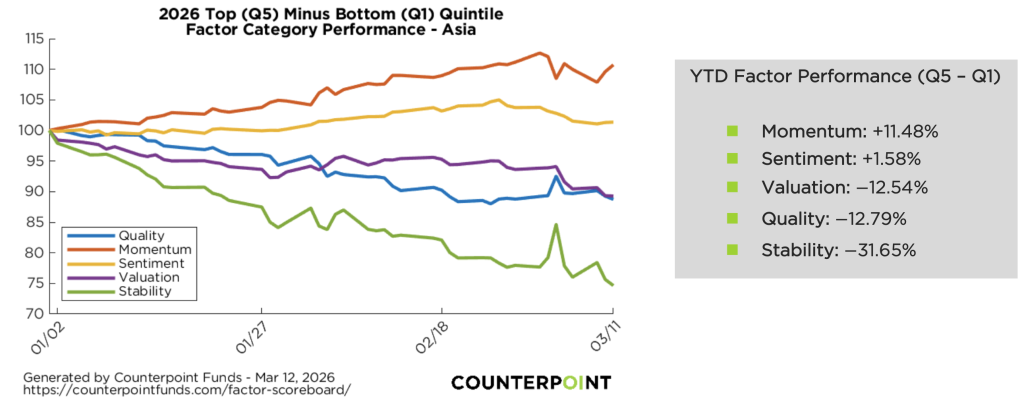

Asia

Asia displays the most extreme factor dispersion among the three regions. Momentum again dominates with a +11.5% return. However, unlike in North America and Europe, quality has underperformed significantly in Asia, producing a −12.8% return, suggesting that lower-quality firms have outperformed higher-quality companies. This dynamic may reflect speculative rotations, policy-driven market moves, or sector-specific recoveries in cyclical industries. Valuation factors also lagged sharply, indicating that cheaper stocks did not outperform expensive ones, despite significant dispersion in earnings expectations across the region. The most dramatic result appears in the stability factor, where low-volatility stocks lagged high-beta stocks by over 30%, signaling a highly risk-seeking market environment.

Cross-Regional Factor Trends

Momentum Dominance

Momentum led in all three regions, with returns ranging from 6% to 11%, confirming that trend persistence remains a major driver of equity returns.

Weakness in Defensive Factors

Low-volatility (Stability) has been the weakest factor globally, particularly in Asia and Europe. This suggests:

- Investors are favoring risk-taking over capital preservation

- Higher-beta equities are leading markets

- Defensive sectors such as utilities and consumer staples may be lagging

Value Struggles

The value/valuation factor remains negative in all regions, suggesting the market continues to favor growth and earnings acceleration over cheap stocks.

Regional Differences

- North America: Balanced factor leadership between momentum and quality

- Europe: Similar trends but with smaller spreads

- Asia: Extreme dispersion with large momentum gains and stability factor underperformance

Key Takeaways for Investors

- Momentum is the strongest factor globally, delivering the largest spreads across North America, Europe, and Asia as stocks with strong recent performance continue to outperform laggards.

- Quality has performed well in developed markets, with profitable, financially strong companies outperforming weaker peers in both North America and Europe year-to-date.

- Sentiment signals have been moderately positive, reflecting improving analyst revisions and investor expectations across multiple regions.

- Valuation (value) factors have lagged globally, as higher-growth and higher-multiple stocks have continued to outperform cheaper equities.

- Defensive and low-volatility stocks have significantly underperformed, indicating strong investor appetite for higher-beta and more cyclical equities.

- Asia shows the greatest factor dispersion, with strong momentum leadership alongside particularly weak performance from defensive and valuation factors.