There is no guarantee that any investment strategy will achieve its objectives, generate profits or avoid losses. Important information about the funds are available in their prospectuses, which can be obtained at counterpointfunds.com or by calling 844-273-8637. The prospectuses should be read carefully before investing. Investors should carefully consider the investment objectives, risks, charges, and expenses of the funds managed by Counterpoint Funds. The Counterpoint Funds fund family is distributed by Northern Lights Distributors, LLC member FINRA/SIPC. Counterpoint Funds, LLC is not affiliated with Northern Lights Distributors, LLC member FINRA/SIPC.

Important Risk Information

Investments cannot be made in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges. Past performance is no guarantee of future results. There is no guarantee that any investment will achieve its objectives, generate positive returns, or avoid losses. The Adviser’s reliance on its strategy and judgments about the attractiveness, value and potential appreciation of particular securities and the tactical allocation among investments may prove to be incorrect and may not produce the desired results. No level of diversification can ensure profits or guarantee against loss.

Mutual Funds involve risk including the possible loss of principal. The fund (and long-short strategies) hold long positions, which entail purchasing securities with the intention of holding them in anticipation of a price increase, and short positions, which entail borrowing securities with the intention of holding them in anticipation of a price decrease. The use of leverage by the Fund or an Underlying Fund, such as borrowing money to purchase securities or the use of derivatives, will indirectly cause the Fund to incur additional expenses and magnify the Fund’s gains or losses. A higher portfolio turnover will result in higher transactional and brokerage costs. Derivative instruments involve risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional investments.

Overall equity and fixed income market risk, including volatility, may affect the value of individual instruments in which the Fund invests. The net asset value of the Fund will fluctuate based on changes in the value of the U.S. and/or foreign equity securities held by the Fund. Fixed income risk factors include credit risk and prepayment risk. When the Fund invests in other investment companies, it will bear additional expenses based on its pro rata share of the other investment company’s operating expenses, including the potential duplication of management fees.

The Fund may invest in options which hold an underlying risk greater than securities. The Fund’s losses are potentially large in a written put transaction and potentially unlimited in an unhedged written call transaction. The earnings and prospects of small and medium sized companies are more volatile than larger companies and may experience higher failure rates than larger companies. The Fund may use swaps to enhance returns and manage risk, which involves risks possibly greater than, the risks associated with investing directly in securities and other traditional investments.

The Adviser’s reliance on its strategy and its judgments about the value and potential appreciation securities in which the Fund invests may prove to be incorrect, including the Adviser’s tactical allocation of the Fund’s portfolio among its investments. The adviser’s investment model carries a risk that the mathematical model used might be based on one or more incorrect assumptions.

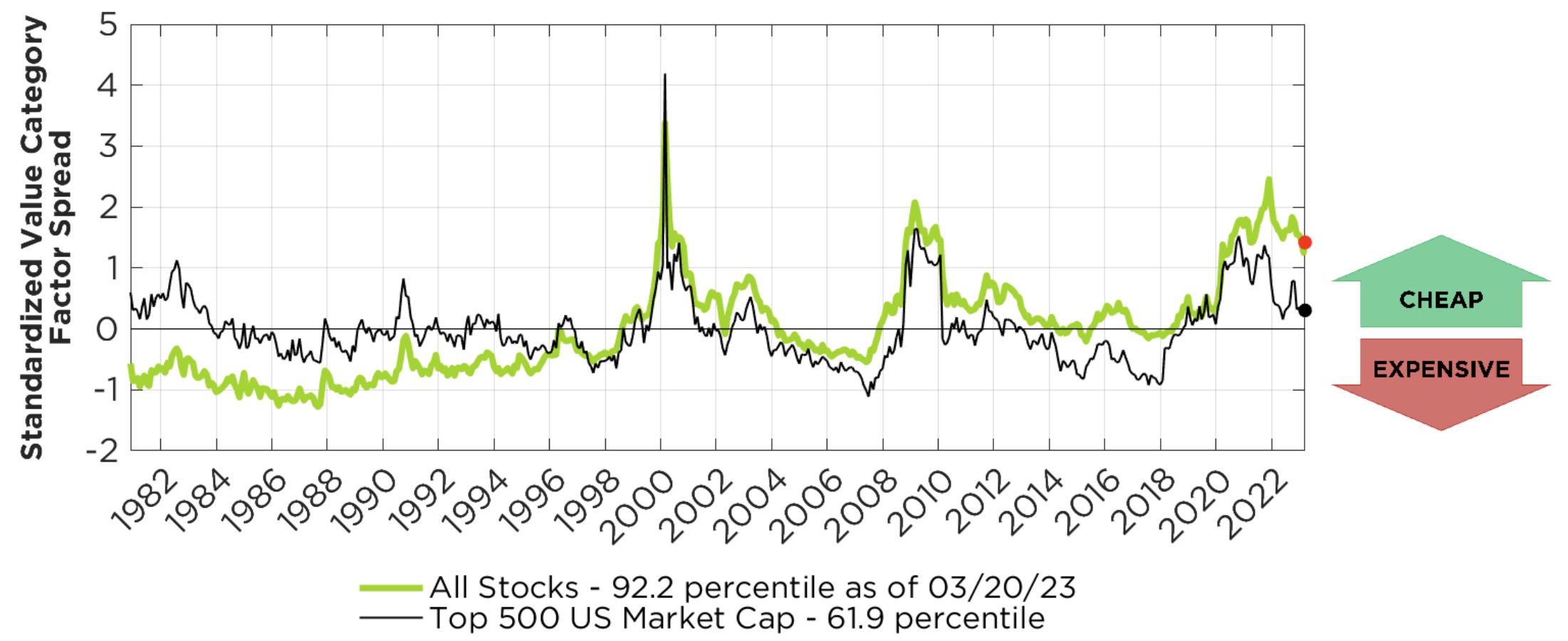

The indices shown are for informational purposes only and are not reflective of any investment. The “Top 500 US Market Cap” subset is defined as the top 500 stocks sorted by market capitalization that trade in the United States which is evaluated on a point in time monthly basis. It is not possible to invest an index. The data shown does not reflect or compare features of an actual investment, such as its objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features. Past performance is no guarantee of future results. There is no guarantee that any investment strategy will achieve its objectives, generate profits or avoid losses.

Factor Spread Methodology

Valuation factor spreads are computed by using four valuation factors: Earnings to Price, Price to Sales, Price to Book, and Cashflow to Enterprise value. Each factor value is sorted within sector, and the top quintile is used to form the “cheap” basket while the bottom quintile is used to form the “expensive” basket. The median value within each basket is taken for every given month in the history. A ratio of these medians is computed on a monthly basis, and that series of ratios is transformed into a standardized z-score, reflecting the normalized variance from the mean historic value at any point in time.

Each factor is equal weighted, and the z-score depicted is an average of the z-score of individual factors. The percentile on each chart is derived from the z-score, assuming normality in distribution of historic measures of ratios of medians. A z-score of 0 would derive a percentile of 50% with this approach, meaning the result is at the historical mean.

Long-only “value of value” is computed identically to the above, except that the absolute value of the median from the top quintile “cheap” basket is not transformed by a ratio against the “expensive” basket referred to above.

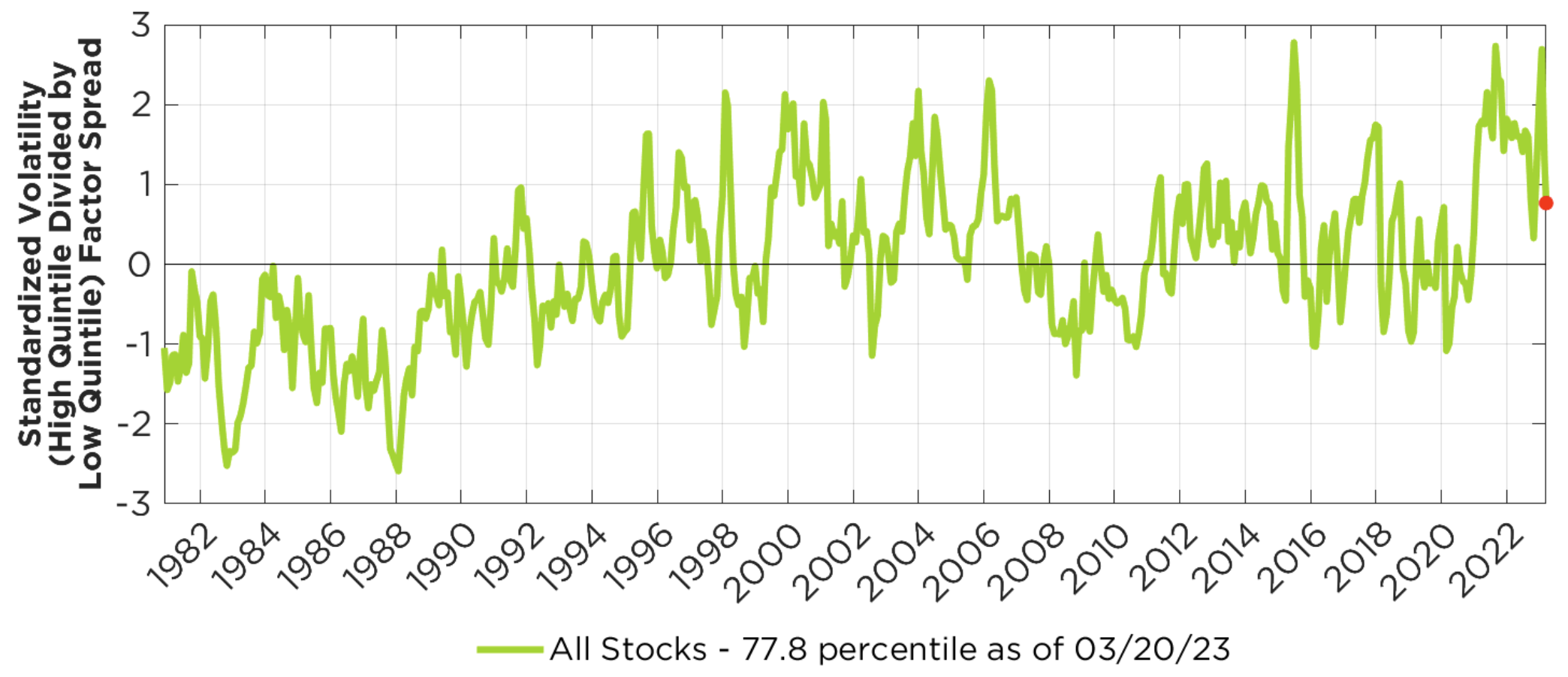

The profitability factor spread utilizes the ratio of gross profits to average company assets. The volatility factor uses 90-day trailing realized volatility to form its sorts.

The methodology for computation of factor spreads of these two factors is the same as above, but only differs that value-related factors are not utilized. The profitability factor is sorted, and the ratio of median of the profitability factor for top and bottom quintiles are computed. The volatility factor is sorted and transformed the same way.

The universe of stocks is represented by global developed, includes no emerging markets, and all valuations imply equal weighting of chosen median values.

Definitions

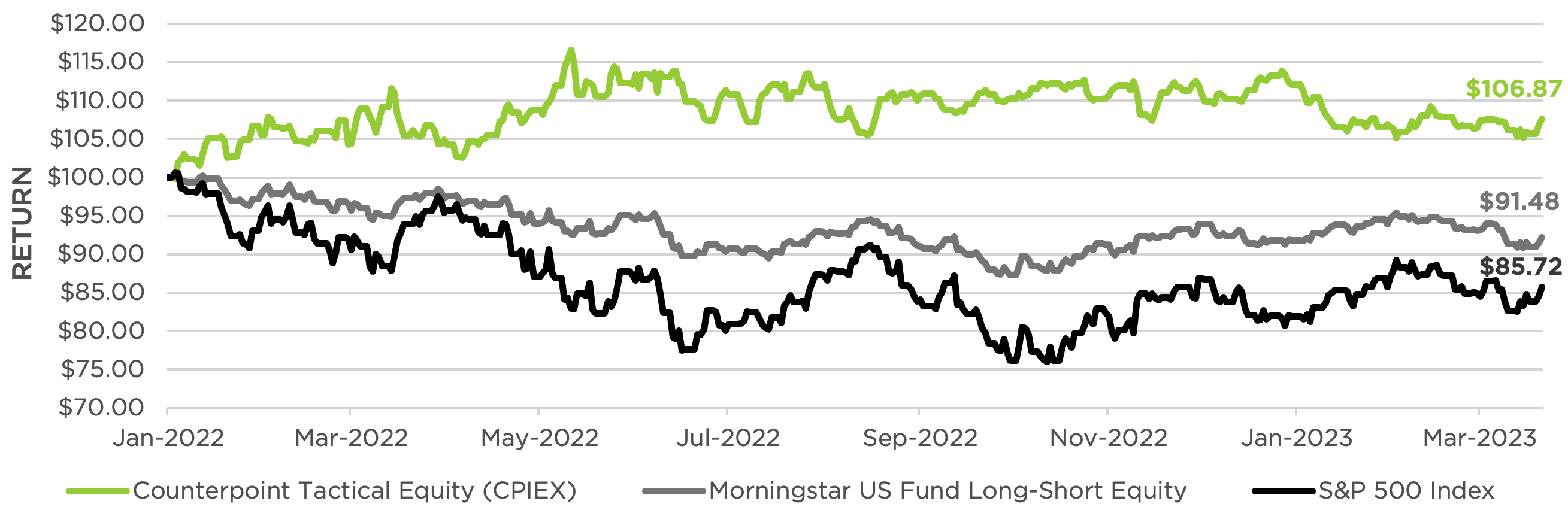

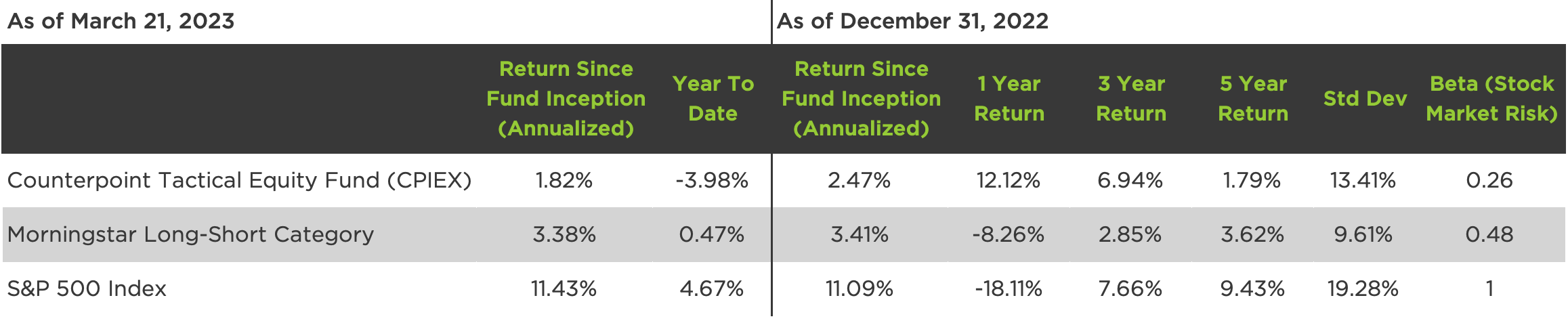

S&P 500 USD includes 500 leading companies in leading industries of the U.S. economy and is a proxy for the total stock market.

Return is the percentage change in the value of an investment, and/or cash flows which the investor receives from that investment, such as interest payments, coupons, cash dividends, stock dividends or the payoff from a derivative or structured product, over a specified time period.

Beta (β) is a measure of the volatility—or systematic risk—of a security or portfolio compared to the market as a whole or index such as the Bloomberg Barclays US Aggregate Bond Index.

Standard Deviation (Std Dev) measures the dispersion of returns relative to its mean to determine the volatility of an investment and is calculated as the square root of the variance by determining the deviation of daily returns relative to the mean.

© 2023 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

5282-NLD-03/22/2023